This post is a work-in-progress, and is still a bit rough around the edges…

Do 1.5°C matter?

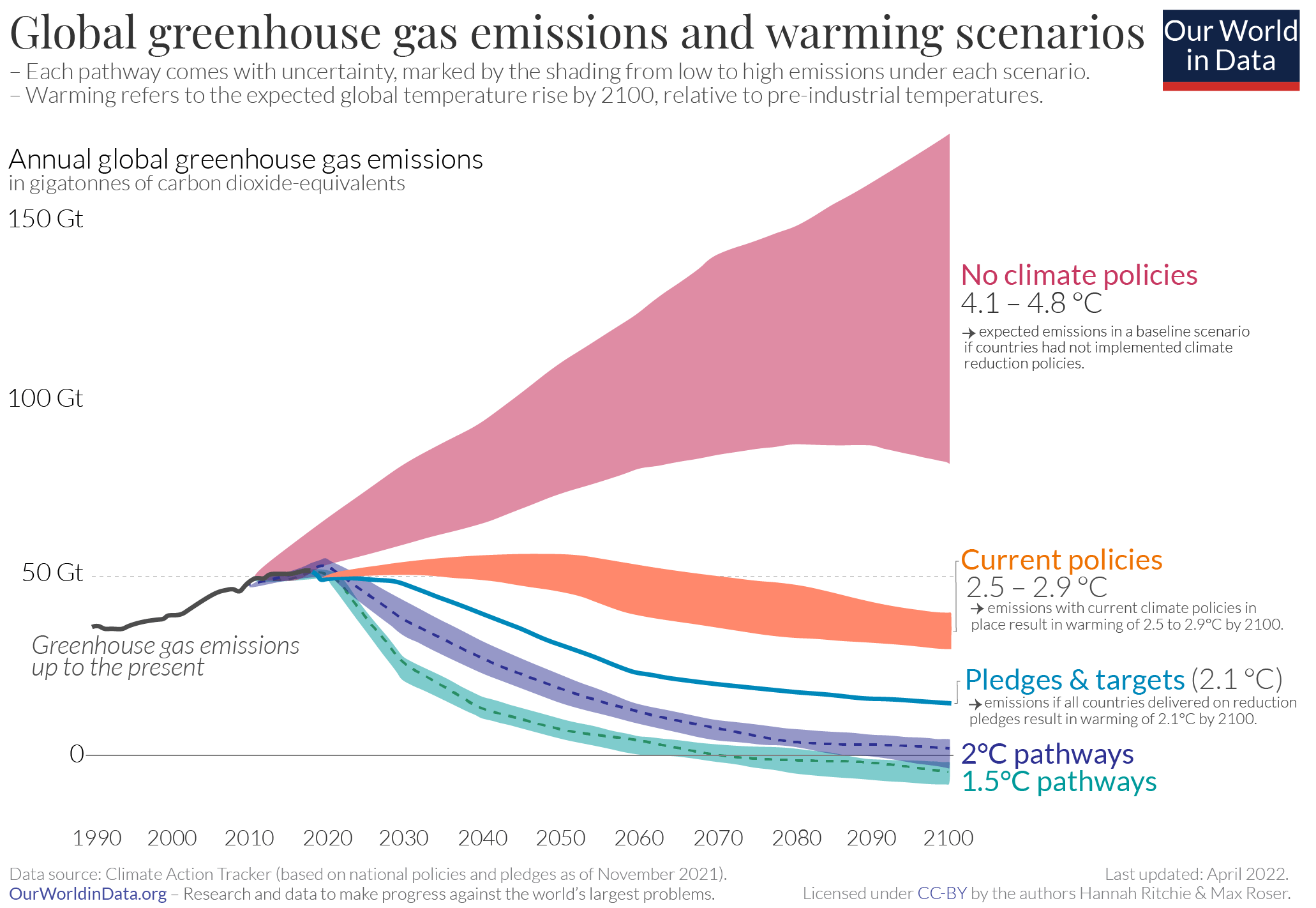

In 2021, at the UN Climate Change Conference (COP26) held in Glasgow, the world reaffirmed its ambition to limit the increase in average global temperatures to 1.5°C above pre-industrial temperatures. This goal, first set at the Paris UN conference (COP15), aimed to prevent the world’s most vulnerable countries from the worst impacts of climate change. For example, at above 1.5°C, it was estimated that 80% of the Maldives’ surface area would find itself below water. Since then, this target has largely been considered as being unachievable, with the UN estimating that this temperature will already be reached in the mid 2030s (i.e. in only 10-15 years’ time), [1] and the UK government estimates that at the current rate, temperatures are due to peak at 2.5-2.7°C above pre-industrial temperatures. [2]

So why the gloomy output? Essentially, the forecast peak warming temperature is a direct consequence of additional net carbon that is added to the atmosphere. The UN estimates that +1.5°C requires no more than a further 500bn tonnes of additional carbon dioxide to be added to the atmosphere. Considering global emissions are running at around 40bn tonnes/year, this leaves only 12-13 years of emissions at the current rate, after which all emissions will have to stop. Clearly, global emissions will not cliff-edge from the current rate to zero. Instead, a pathway to an acceptable peak temperature will require a glide path to reducing global emissions, while at the same time introducing mechanisms to remove carbon from the atmosphere. When carbon emissions and removals balance out, we will have reached ‘net zero’, and global temperatures will stop rising.

The Climate Tech Landscape

So how does the ever-burgeoning set of companies calling themselves a Climate Tech or Clean Tech company fit into this outlook? Any company describing itself as being a climate tech company should be directly or indirectly contributing towards the reduction of net emissions. There are two principal ways in which it can be achieved. The first is to directly influence the amount of carbon in the atmosphere, either by improving the carbon efficiency of existing processes, by providing a non-carbon alternative, or alternatively by removing carbon from the atmosphere. We shall call this the carbon reduction category. Then there is then a swathe of companies that provide climate or carbon intelligence, all of which provide insight into the emissions and climate impact across companies, territories or industries. Whilst these companies are not directly involved in carbon reduction, the insight is critical for appropriate targeting of efforts, auditing their impact, and pricing the cost of carbon. There is also a third category of companies aiming to help organisations adapt to the impact of climate change. Whilst crucial in coping with the impact of warming, these companies do not offer direct or indirect means to lower the peak temperature increase and so I will not consider them further in this post.

Carbon Abatement

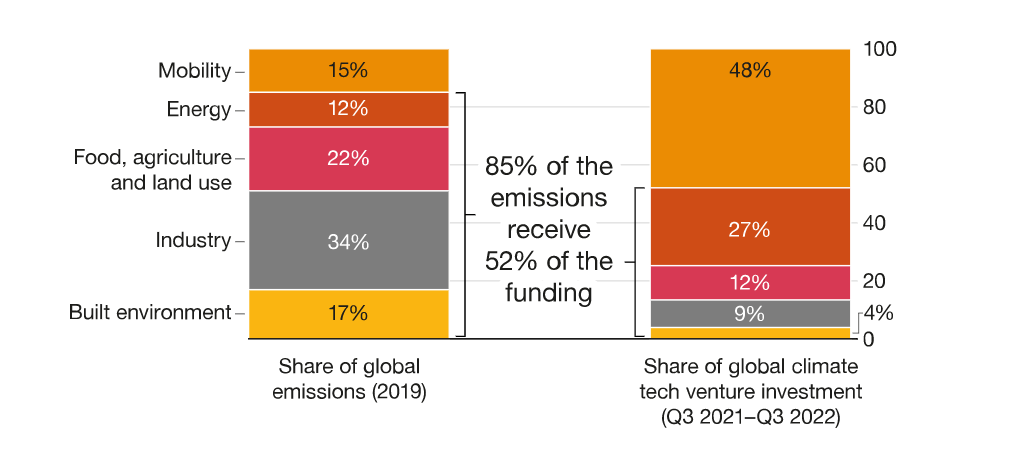

PWC, the accounting and consultancy firm, publishes an annual ‘State of Climate Tech’ report [3]. This report looks at individual emission-generating sectors and assesses the climate tech funding attracted by each sector. These sectors are transport & mobility, energy, food & land use, industry & manufacturing, the built environment and financial services. Additionally, it classifies carbon capture, removal and storage as its own category. This categorisation is pretty common in this space, so I will use it for the remainder of this blog post.

Mobility and Transport is probably the sector that receives the most attention across the tech industry, predominantly through the activities to provide an infrastructure to electrify private and commercial road transport, though also includes efforts to decarbonise sea and air transport. Tesla is the poster child for the electric vehicle (EV) industry, but the entire automotive industry is being electrified, with VW predicting to shift more EVs than Tesla by 2024-5. Companies in this sector are involved in the entire supply chain, from batteries, their supply chain, through to in-home and public charging infrastructure. Indeed, the PWC report indicates that although mobility and transport are responsible for 15% of all global emissions, they receive 48% of global climate tech venture investment. Now, of course, VC funding is only part of the financing available, as SPAC funding, corporate venturing, innovation agencies and other forms of finance are significant contributors, but this figure is indicative of the interest that this sector provides.

Energy generation is going through a wholesale transition towards renewable generation, with 40% of the UK’s electricity now being produced from renewable sources. Although this is, by definition, zero-emission, many renewable energy sources have irregular generation patterns, dependent on when the wind blows or when the sun shines. This provides challenges in the creation of a steady, predictable source of electricity that matches demand, especially as gas, oil and coal power stations are progressively taken offline. In other words, they are not ‘dispatchable’ sources that can be dialled up and down to meet demand. Most climate tech companies in this space aim to address how to bridge this gap, either by (1) providing new, more controllable or predictable energy sources, such as green hydrogen or geothermal energy capture, or (2) by better managing energy generation, distribution and consumption, or finally by (3) introducing energy storage solutions, to help balance supply and demand.

Energy management is attracting a lot of attention from the tech scene, as it is the space most suited to be solved by software solutions. In a nutshell, these involve integrating consumers of energy, such as commercial premises, home heating systems, vehicle charging and so on with energy distributors and producers to adjust demand to better match the supply patterns. Examples include using electric cars to return energy to the grid (Vehicle-to-Grid) or to the home (Vehicle-to-Home), making use of smart home integration to manage electricity demand to better match supply, and introducing price signals to consumers of energy so that they can shape consumption around when energy costs are lowest. Octopus Energy, a UK-based energy utility, offers an electric vehicle tariff called Intelligent Octopus that integrates with the EV’s cloud-based charging APIs to schedule charging when demand is lowest and cost lowest. Amongst the companies supported by Y Combinator is Enode, a Norwegian company that provides energy companies, utilities and grid operators with access to a broad range of smart energy devices such as home chargers, electric vehicles, solar inverters in order to help match demand to their supply.

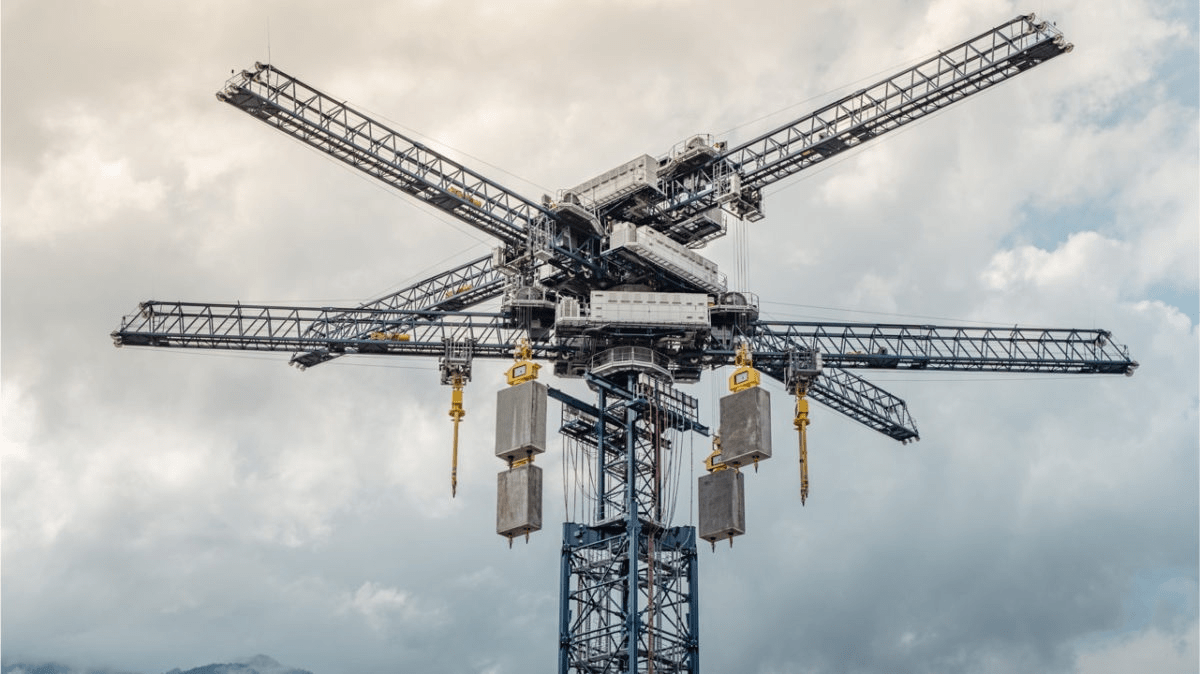

However, software solutions to match supply and demand will only go so far in compensating for the erratic power output patterns of renewable energy. To bridge periods when the wind stops blowing or the sky is overcast, cost-efficient long-duration storage is required. One, slightly unconventional approach is the use of gravitational storage towers that use surplus energy to lift concrete blocks, and return the energy back to the grid by releasing the blocks back down in a controlled fashion. Unlike battery storage, there is no energy loss over time (unless the blocks fall!). Other solutions being developed include solid state batteries, such as lithium-ion tech as used in EVs, flow batteries, and green hydrogen storage.

Agriculture and food production is an often under-recognised source of atmospheric carbon, and is responsible for 26% of global carbon emissions. This is largely driven by the inefficiencies of converting plant protein to animal protein, the large land areas required for livestock and its associated methane emissions. (yes, I mean flatulence). Alternative foods led much promise, but these are dropping off the menu. Even when scaled, cultured meat is estimated to cost more than $63 a kilo to produce, compared to US wholesale prices of $4 and $6 a kilo for pork and beef respectively. This has had an impact on the sector’s outlook. Beyond Meat, one of the stock markets’ darlings in this space has seen its share price drop by 95% since its peak shortly after its NASDAQ IPO in 2019. Vertical and urban farming has long been seen as the future of agriculture, as it is significantly more land-efficient than its conventional counterpart. Infarm, a European vertical farming company that had raised $600m in venture capital, laid off half of its workforce in November, largely due to the increase in energy costs triggered by Russia’s invasion of Ukraine, which has exposed a very high susceptibility to energy prices for these businesses. In truth, it does seem counter-intuitive that the future of farming should dispense with the free solar energy available on tap.

Energy used in commercial and residential buildings contributes to over 17% of greenhouse gas emissions, primarily for heating and cooling (HVAC) as well as lighting and other electricity consumption. Although a lot of attention is brought to creating green buildings, it is clearly more efficient to improve the emissions of the existing building stock built up over the past hundred-plus years. This is the space where the Internet of Things comes into its own, bringing sensors that monitor occupancy, temperature, humidity, solar irradiation, and air quality and coupled with machine learning models to reduce the energy burden of operating buildings. In countries where the pandemic has resulted in hybrid work patterns, utilisation of both offices and homes is now a lot more variable, leaving a lot of optimisation potential in how energy is used. Furthermore, the recent increase in energy costs has improved the return on investment for smart building management systems (BMS).

To be continued. Coming up next

This post has looked at how Clean Tech companies can directly help add or remove carbon from the atmosphere. Part 2 will consider the impact of carbon capture and storage technologies, as well as the role carbon and emissions analytics companies have in targeting efforts to the right area and auditing their impact. I will also touch on the contentious topic of greenwashing and the impact the increasing energy costs are likely to have on the overall Clean Tech Sector.

Further Reading

Analysis: What the new IPCC report says about when world may pass 1.5C and 2C

UK Climate Change Committee, “COP27: Key outcomes and next steps for the UK”

Y Combinator, “Request for Startups: Climate Tech”, December 2022

David Rusenko, “Proposal: A founder-focused climate tech taxonomy”, December 2022

TechCrunch, “Climate tech is not doomed, despite climate doom”

Wired, Vertical Farming has found its fatal flaw, November 2022

Energy Storage News, “Long duration energy storage to scale in second half of 2030s”, October 2022

The post Climate Tech – Is it all Greenwashing? appeared first on The Sand Reckoner.