The history of computing has been a multi-decade case study of network effects. When a product benefits from a network effect, its value to its customers increases as the number of buyers or sellers using it increases. The dominance of the Windows PC operating system was a classic case. By providing a ‘compatible platform’ for personal computers, software developers could reach millions of users, and the personal computing revolution took off.

Network effects came to play in the current generation of the Web, sometimes referred to as Web 2.0. The first incarnation of the web, which was built on open standards, including HTML, SMTP email, this iteration was basically an interoperable global noticeboard, making information available over the Internet. There were a plethora of search engines, each quickly making its predecessor obsolete. Remember Alta Vista, HotBot, Ask Jeeves? There was no ‘stickiness’ inherent to any of these services, which meant that the moment one search engine out-performed the previous, users would immediately shift. Then the early 2000s then saw the advent of Web 2.0, sometimes referred to as the ‘Social Internet’, where many new companies such as MySpace, LinkedIn, DropBox, Blogger, Facebook, Twitter etc. began creating web experiences that were interactive and personal. By holding information about their customers, they were able to create and tailor experiences that were personal to them, thereby creating stickiness. Google then showed the world how to create a very valuable advertising business using the personalisation it was hoovering up from its customers. This marked the return of network effects, and increased market concentration and centralisation. A platform was now valuable to its users only if their friends and colleagues were on it, and was valuable to other businesses only if it could link to enough customers.

Blockchain and Web 3.0

So why this quick ramble through the Internet’s potted history? Well, the next purported evolution, referred to unoriginally as Web 3.0, or simply Web3, promises to make use of crypto technologies to break the stranglehold of concentration of the big tech players. So is this the next big thing, or simply pie in the sky?

For an outsider, the numbers relating to cryptocurrencies are somewhat bewildering. From the capitalisation of the cryptocurrency market (it reached $30 trillion at the end of 2021), to its high volatility (it has since lost two-thirds of its value), it is difficult to get one’s head as to what is really going on. Despite being variously compared to a modern-day Ponzi scheme that would make Bernie Madoff blush, smart people are still betting big money on crypto tech.

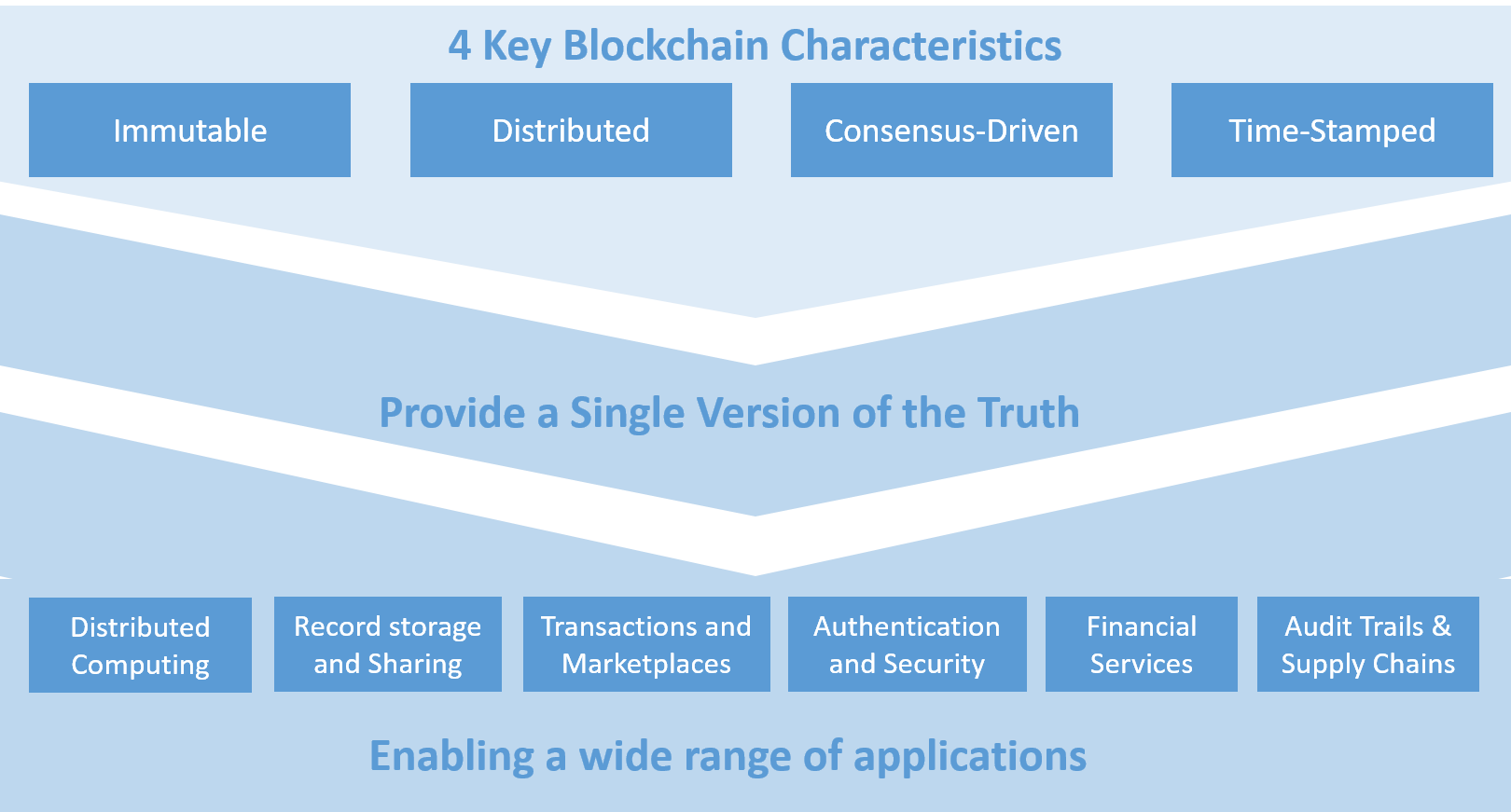

In a previous post, I looked at the applications of blockchains, the technology that underpins cryptocurrency, showing how clever cryptography can provide a single version of a ‘truth’ that does not rely on the data or certification being provided by a single party, but instead is based on a decentralised network of several parties, all of whom have a stake in the system.

The Case for Web3

Andreessen Horowitz, also known as a16z, is a legendary Silicon Valley venture capital firm, whose founders were early investors in Facebook, Twitter, GitHub, Stripe, Waymo, AirBnB and Roblox. In May, it announced that it raised $4.5 billion for a crypto fund. Chris Dixon, who leads a16z’s crypto investments says that decentralisation and crypto are the new frontiers for 16z investment, as it fuels entrepreneurship, and pushes back away from the intrinsic centralisation of Web 2.0 companies. As an example, he explains how the proceeds of virtual goods in Fortnite go to the company behind the game. Instead, the sale of Non-Fungible Tokens (NFTs) is a means for creators to sell assets directly to a fanbase, in order to monetise that fanbase. According to Dixon, Web3 allows creative people, businesses and startups to reach audiences directly and have a relationship “that is not mediated by algorithms and advertising.”

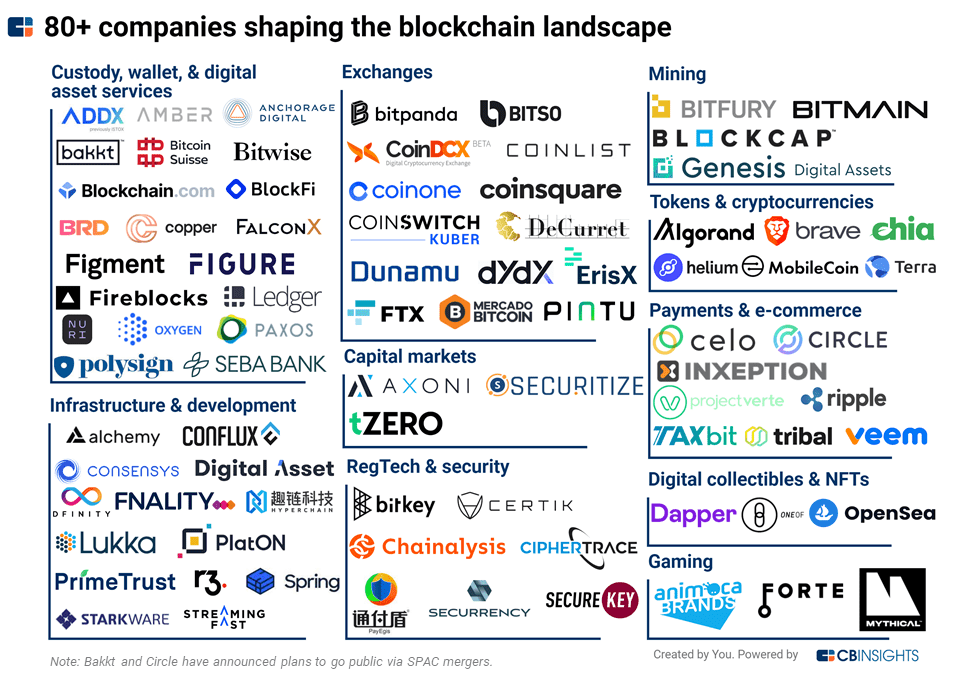

The likes of a16z and other investors are fueling a burgeoning ecosystem of tech companies that are working to provide the building blocks to deliver on the Web 3.0 vision. Some of these are busy creating the building blocks of a Web3 infrastructure, including the blockchains themselves, including their crypto algorithms, the nodes that host the ledgers, and tooling and services that interconnect between blockchains and provide a variety of crypto-as-a-service applications. On top of these are the Web 3 applications, including Circle, which provides companies with the ability to transact financially with multiple cryptocurrencies, Sky Mavis, who provide the building blocks for creating decentralised online games, where all users can transact and sell game items, and OpenSea, a market place for peer-to-peer NFT transactions.

The Opportunities

When looking at Web3, a couple of key opportunities stand out. Decentralised Finance, also known as DeFi, whilst in its infancy, clearly will act as a spur to innovation in the broader finance industry. and possibly reconfigure the finance industry. Banks, wire transfer companies and payment networks all act as centralising conduits, extracting rents of anything between 1-4% on the value transacted, with operating margins in the order of 60-80%. These fees mean that established institutions are vulnerable to disruption by lower-cost crypto networks. Already in 2021, the value of transactions underpinned by Ethereum, one of the largest blockchain networks was $6 trillion. By comparison, Visa handled $10.14 trillion worth of transactions that year. The use of smart contracts, agreements that are automatically enforced and cannot be tampered with can be used to support a wide range of transactions, the crypto equivalent of shares, loans and ‘stablecoins.’

Non Fungible Tokens are unique records of digital assets that can be exchanged or sold, usually using cryptocurrencies that prove ownership of that digital assets. As they live on open blockchains, normally Ethereum, their transaction history is visible to all. Moreover, digital creators can retain a stake in their work, for example by retaining a share of the proceeds on any future resales enforced by smart contracts. Digital assets range from tweets, digital football trading cards, magazine articles or video game assets. Although the market for NFTs has tanked recently, for as long as artists continue to create digital content, be they music, visual, or gaming content, then it is likely that NFTs, or something like them, will be used to create a market where they can be bought and sold.

The Challenges to be Overcome

Having seen a fair few tech cycles, the extent of fragmentation of the Web3 landscape means that it feels a few years at best from going mainstream. Despite a16z’s enthusiasm, the computer industry does appear to have a tendency towards centralisation, rather than decentralisation.

Consider online music. Decentralised peer-to-peer services such as Napster and Kazaa provided listeners the world over with free, nearly limitless music, shared through PC applications across the world. Although these p2p applications provided access to music, the experience was poor. Slow, unreliable, with a clunky user interface. It was almost as though there wasn’t a single product development creating the experience! Then, in 2008, Spotify demoed their fledgling PC application to Universal, based on a tech stack that they developed with the sole purpose of cloud-based music streaming. Not only had music streaming made the jump from a hacky tech enthusiast’s tool to an application that anyone could use, but the music labels now had a partner with who they could set up contracts and hopefully build a sustainable business model.

The centralised services that Web3 advocates say get in the way between creators and their fans, such as recommendation algorithms and advertising, are what generate awareness in the first place. For example, Sam Ryder, who sang his way to a run-up position in this year’s Eurovision, could certainly drive up a sustainable business through selling access and digital assets as NFTs. But would that have been possible without TikTok’s recommendation algorithm which catapulted him from being an unknown artist singing covers from home over lockdown to a viral sensation with nationwide name recognition?

Similarly, for all the decentralising architecture of DeFi, there remain centralised control points. For example, online wallets that allow users to buy, sell and manage crypto assets manage passwords and logins on their users behalf, just like traditional online services. So what does Web3 need to achieve if it is truly to become mainstream?

Energy Efficiency

This is one area where there has been significant progress lately. Until recently, the Ethereum blockchain required approximately 4.8kWh for its ‘proof of work’ algorithm, which is more than the UK’s daily household electricity consumption. Think about it. A single online transaction requires more electricity than the domestic appliances, lighting and varied electricity needed by a family for a whole day. Particularly as much of the world faces an energy cost crisis, this was unsustainable. Ethereum claims that this was addressed in an upgrade called ‘The Merge’ which took place on, moving its verification algorithms to a system called ‘proof of stake’ which is a lot more efficient (Ethereum claims that energy consumption will decrease by 99.95% per transaction). For a comparison between these two algorithms, see here.

Be accessible to a non-tech customer base

First crypto transactions need to become more user-friendly, particularly for people who don’t care about the underlying tech. You don’t for example need to care how a car works, to want to drive one. The Verge quotes an example where some NFTs priced at $198,000 sold for $1,800 because some older online listings were still active. As blockchain transactions are irreversible, there was no way for the sellers to recover or reverse the transaction. As there was no intermediary in place who would guarantee or underwrite the sale, the asset was gone. Similarly, crypto wallets that allow users to hold their own private keys have no dependency on an online service, but if the user loses them, they are gone forever, much like cash under the mattress. This leads to the question, “Who do customers go to when things go wrong?” As anyone involved in creating consumer experiences knows, you can only really delight customers if you are able to deal with all the range of ways in which your service can go wrong. In this case, blockchain immutability is a challenge.

Prevent Abuse and Harassment

As blockchain platforms effectively provide exchanges for often anonymous users, there are currently few ways by which illicit, discriminatory, offending or otherwise illegal material can be revoked. The immutability of the transactions, the anonymity behind crypto wallets, the ability to obfuscate the source and destination of funds, plus the intrinsic openness and visibility of the ledgers cause all sorts of problems. A blog on the topic explored the ramifications of the transparency of public transactions, looking at the risks from abusive partners, harassment, revenge porn and so on. There seems to be little thought across the industry on how these issues will be addressed. After all, one of the strongest advantages of centralised systems is that it is clear who legislators and law enforcement authorities can go to in order to put things right.

Interoperability

Any financial asset that has a realisable value must be ‘liquid’, in other words, it should be able to be converted to another form of asset. For example, a house can be sold for cash. If it cannot be sold, it is illiquid, and hence has no financial value. For this very fundamental reason, all financial products and transaction platforms, allow for the transfer or conversion of assets. This is the financial equivalent of interoperability in the tech world. While the Web was built on a fully standardised set of technologies that we take for granted, (albeit with limited interoperability between, different platforms – Facebook, Tiktok etc), the blockchain networks on which Web3 is built are completely siloed. A digital asset such as an NFT held on one blockchain, say Ethereum, cannot easily be transferred onto another one, such as Solana. Similarly, the applications that run on given blockchains are also their own islands. Today this is being addressed through specific bridges between different applications, but this is a non-scalable solution that also introduces intermediary choke points that undermine the decentralised vision. Until protocols and asset formats become standardised, just as emails can be sent seamlessly across different email providers, then anyone using a Web3 application will be locked-in to whatever application or platform they selected.

Conclusion

While cryptocurrencies will likely become an increasingly important part of the fintech fabric, and blockchains will continue to find a diverse range of applications, decentralisation is something that will happen by degree. Bringing creators and consumers together requires often requires multi-sided platforms and companies to operate them. The scale that TikTok, Facebook or Google provide, also provides convenience, as it makes it easier for people to find the experiences, content or people they are looking for. Fully decentralised networks are also, by definition, fragmented, which will create significant usability issues that would likely be too high a barrier for mass market adoption. As the tech improves, as networks and blockchains become increasingly interoperable, regulators will also insist that there are legal entities who can take accountability for what takes place on a blockchain. For these reasons, I think it is more likely that the crypto tech underpinning Web 3.0 will be embraced by both existing and emerging tech companies as a way of providing customers with greater control and ownership over their own data, more transparency on how it is used and allowing faster and cheaper transactions. Along the way, we also doubtlessly see existing business models perishing and new ones emerging.

Further Reading

The Future According to Andreessen Horowitz, CB Insights (registration required)

Engineering at Spotify, “What we learned from creating Spotify’s desktop app”

The Verge Podcast, “Chris Dixon thinks Web3 is the Future of the Internet – Is it?”, April 2022

ArsTechnica, “Ethereum completes The Merge”, 21 September, 2021

The Verge, “Three Things Web3 should fix in 2022,” 28 Jan 2022

“The Crypto World Can’t Wait for ‘the Merge'”, New York Times, 26 August 2022

VentureBeat, “Interoperability must be a priority for building Web3 in 2022”, 12 February, 2022

The post Web3 – The promise of a decentralised web appeared first on The Sand Reckoner.